](https://file-host.link/website/levelsolutionsusa-18nvd9/assets/blog-images/97c39004-5b03-45ac-9cc3-7326ecddb241/1771466863131769_7778ca8d054842109f25b9e5afb91d27/360.webp)

Introduction

The U.S. semiconductor industry generates over $318 billion in annual revenue and commands more than 50% of the global market. This dominance makes American chip production essential to national security, technological innovation, and economic competitiveness.

These chips power everything from AI data centers and autonomous vehicles to defense systems and telecommunications infrastructure. U.S. companies lead in design, intellectual property, and advanced manufacturing equipment.

The CHIPS and Science Act has triggered a manufacturing renaissance, driving over $640 billion in private investments to expand domestic production capacity. This legislation aims to triple U.S. chipmaking capacity by 2032 and increase the domestic share of advanced logic manufacturing from virtually zero to 28%.

This addresses decades of offshore manufacturing migration while securing critical supply chains.

TL;DR

- U.S. semiconductor companies generate $318 billion annually, holding 50% global market share despite only 12% of manufacturing capacity

- Fabless designers (Nvidia, AMD, Qualcomm) and integrated manufacturers (Intel, Texas Instruments) lead the industry

- CHIPS Act investments exceed $640 billion, funding new fabs from Intel, TSMC, Samsung, and Micron across Arizona, Texas, and Ohio

- Authorized distributors provide inventory buffering, technical support, and mil-spec compliance for procurement teams

- U.S. manufacturers lead in AI accelerators, mobile processors, analog chips, and semiconductor equipment despite overseas production reliance

Overview of Semiconductor Manufacturing in the United States

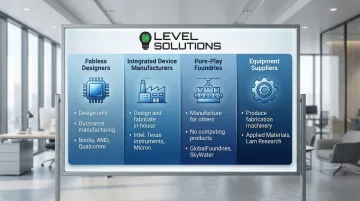

The U.S. semiconductor ecosystem encompasses four distinct business models, each playing a critical role in the supply chain:

Business Model Breakdown

- Fabless designers create chip architectures and intellectual property but outsource all manufacturing to third-party foundries (examples: Nvidia, AMD, Qualcomm, Broadcom)

- Integrated device manufacturers (IDMs) design and fabricate their own chips in company-owned facilities (examples: Intel, Texas Instruments, Micron)

- Pure-play foundries manufacture chips designed by other companies without competing products (examples: GlobalFoundries, SkyWater Technology)

- Equipment suppliers produce the specialized machinery required for chip fabrication (examples: Applied Materials, Lam Research, KLA Corporation)

Current Manufacturing Landscape

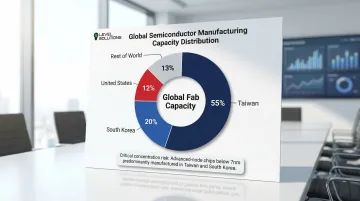

While U.S. companies lead globally in semiconductor revenue (50.4% market share) and design innovation, domestic manufacturing capacity represents only 12% of global production. The concentration of global production creates critical vulnerabilities:

- Taiwan controls approximately 55% of worldwide fabrication capacity

- South Korea holds another 20% of global production

- Advanced-node chips below 7 nanometers face highest supply chain risk

The CHIPS and Science Act allocates $52.7 billion to address this imbalance—$39 billion for manufacturing grants and loans, $11 billion for R&D, and $2 billion for workforce development.

The legislation aims to reverse four decades of manufacturing decline and establish the U.S. as a leader in both chip design and production by 2032.

Understanding which manufacturers drive this resurgence requires examining their technological capabilities and market positions.

Top U.S. Semiconductor Manufacturers and Component Suppliers

Companies were selected based on revenue scale, technological innovation, manufacturing footprint, and strategic importance to U.S. supply chains across commercial and defense applications.

Nvidia Corporation

Nvidia transformed from a gaming graphics card company to the world's most valuable semiconductor firm, capturing over 85% of the AI accelerator market. The company's fabless model outsources all manufacturing to TSMC and Samsung while maintaining complete control over chip architecture and software ecosystems.

Nvidia holds approximately 85% market share in AI accelerators, with its H100 and Blackwell chips powering generative AI systems at Microsoft, Meta, Amazon, and Google.

| Category | Details |

|---|---|

| Headquarters & Business Model | Santa Clara, CA; Fabless semiconductor designer (outsources manufacturing to TSMC and Samsung) |

| Key Products & Specializations | AI accelerators (H100, Blackwell chips), GPUs for gaming and data centers, automotive computing platforms (DRIVE), professional visualization |

| Market Position & Revenue | Market cap: $4.45 trillion; TTM Revenue: $125.7 billion; 85% market share in AI chips; partnerships with all major cloud providers |

Why Nvidia stands out:

- First semiconductor firm to surpass $100 billion in annual revenue, driven by AI data center demand

- CUDA software platform makes it difficult for customers to switch to competing chips

- Dominates AI accelerator market even as AMD develops alternative offerings

Intel Corporation

Intel pioneered the microprocessor revolution and remains the largest U.S.-based chip manufacturer with extensive domestic fabrication facilities. Unlike fabless competitors, Intel designs and manufactures chips in-house across 12 U.S. fabs in Arizona, Oregon, New Mexico, and Ohio.

The company received $7.86 billion in CHIPS Act grants plus $11 billion in loans—the largest single award—to expand advanced manufacturing and launch Intel Foundry Services as a contract manufacturer competing with TSMC and Samsung.

| Category | Details |

|---|---|

| Headquarters & Business Model | Santa Clara, CA; Integrated Device Manufacturer (designs and manufactures chips in-house) plus foundry services |

| Key Products & Specializations | CPUs for PCs and servers (Core, Xeon families), GPUs (Arc), foundry services, memory and storage solutions, automotive chips |

| Manufacturing Presence & Investment | 12 U.S. fabs; investing $100+ billion in Arizona and Ohio facilities; government holds 10% equity stake; targeting Intel 18A process node by 2025 |

Why Intel stands out:

- One of only two companies (along with Samsung) manufacturing leading-edge logic chips domestically

- Operates foundry business for external customers while producing its own designs

- $3 billion Secure Enclave award highlights strategic importance to defense supply chains

Qualcomm Incorporated

Qualcomm's Snapdragon processors power the majority of premium Android smartphones worldwide. The San Diego-based fabless designer pioneered CDMA wireless technology and holds extensive patent portfolios in 5G, generating significant licensing revenue beyond chip sales. Qualcomm is rapidly expanding into automotive semiconductors with its Snapdragon Digital Chassis platform, targeting electric vehicles, advanced driver assistance systems, and in-vehicle infotainment.

| Category | Details |

|---|---|

| Headquarters & Business Model | San Diego, CA; Fabless semiconductor designer (outsources to GlobalFoundries, Samsung, TSMC) |

| Key Products & Specializations | Snapdragon mobile processors, 5G modems and RF systems, automotive platforms (Digital Chassis), IoT connectivity solutions, Wi-Fi and Bluetooth chips |

| Market Position & Applications | TTM Revenue: $33.2 billion; Market cap: $159 billion; Serves mobile, automotive, IoT, industrial, and edge computing markets |

Why Qualcomm stands out:

- Leadership in 5G technology and RF front-end systems provides strong competitive advantages

- Extensive patent portfolio generates licensing revenue beyond chip sales

- Automotive expansion targets EV market where chip value per vehicle will exceed $1,500 by 2030

Texas Instruments

Texas Instruments operates as one of the world's largest analog semiconductor manufacturers, with a 70-year history dating to the invention of the integrated circuit. Unlike digital logic chips that process binary data, TI's analog chips manage real-world signals—power, temperature, sound, and light—across 80,000+ products serving industrial and automotive markets.

The company operates eight U.S. fabrication facilities and is investing $11+ billion to expand domestic 300mm wafer production, which delivers approximately 40% lower costs per chip compared to older 200mm processes.

| Category | Details |

|---|---|

| Headquarters & Business Model | Dallas, TX; Integrated Device Manufacturer with 8 U.S. fabrication facilities (Texas, Utah, Maine) |

| Key Products & Specializations | Analog chips, embedded processors, power management ICs, amplifiers, data converters, voltage regulators for industrial and automotive applications |

| Manufacturing & Customers | TTM Revenue: $17.68 billion; Market cap: $205 billion; CHIPS Act recipient ($1.6B grants); building new 300mm fabs in Utah and Texas; supplies Dell, HP, Apple, Cisco |

Why Texas Instruments stands out:

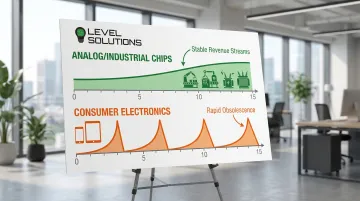

- Focus on analog and embedded processing serves markets with 10-15 year product lifecycles

- Longer lifecycles provide stable revenue streams compared to 2-3 year consumer electronics cycles

- Commitment to domestic manufacturing strengthens U.S. supply chain resilience for industrial and automotive sectors

Advanced Micro Devices (AMD)

AMD staged one of the semiconductor industry's most remarkable comebacks, reclaiming market share from Intel in CPUs while simultaneously challenging Nvidia in AI accelerators. The company's fabless model—adopted after spinning off manufacturing operations as GlobalFoundries in 2009—allows AMD to leverage TSMC's leading-edge process technology without massive capital expenditures. AMD's EPYC server processors power data centers at Microsoft Azure, Google Cloud, and AWS, while its MI300X AI accelerators compete directly with Nvidia's H100 in large language model training.

| Category | Details |

|---|---|

| Headquarters & Business Model | Santa Clara, CA; Fabless designer (manufacturing outsourced to TSMC and Samsung) |

| Key Products & Specializations | Ryzen CPUs for desktops and laptops, EPYC data center processors, Radeon GPUs for gaming, MI300X AI accelerators for machine learning workloads |

| Market Position & Strategy | TTM Revenue: $34.6 billion; Market cap: $338 billion; Data center revenue up 32% in 2025; revenue-sharing agreement with U.S. government for AI chip sales to China |

Why AMD stands out:

- Chiplet architecture connects multiple smaller dies, improving yields and reducing costs while maintaining performance

- Only company competing with both Intel (CPUs) and Nvidia (AI accelerators) in high-performance computing

- EPYC processors power data centers at Microsoft Azure, Google Cloud, and AWS

How We Chose the Best U.S. Semiconductor Manufacturers

Company selection prioritized revenue scale, technological leadership, manufacturing presence, and strategic importance to U.S. supply chains. A common mistake in semiconductor procurement is confusing chip manufacturers with component distributors—manufacturers design and fabricate chips, while distributors stock and distribute those components to end users.

With this distinction in mind, we evaluated manufacturers using these criteria:

Evaluation Criteria:

- Financial performance: Revenue exceeding $15 billion annually and market capitalization reflecting long-term viability

- Innovation leadership: Patents, process node advancement, and market share in high-growth segments (AI, automotive, 5G)

- Domestic manufacturing: U.S. fabrication facilities and CHIPS Act participation showing commitment to domestic production

- Product portfolio breadth: Serving multiple markets (consumer, industrial, automotive, defense) to ensure supply chain relevance

Understanding the Semiconductor Ecosystem

The semiconductor ecosystem includes three key player types:

- Manufacturers create and fabricate chips at scale

- Equipment suppliers build fabrication machinery

- Distribution partners bridge the gap between manufacturers and end users

Manufacturers focus on design and high-volume production. Distributors maintain inventory, provide technical support, and offer flexible order quantities for businesses that don't require direct manufacturer minimums.

Conclusion

U.S. semiconductor manufacturers remain global leaders in chip design, artificial intelligence hardware, and manufacturing equipment despite four decades of offshore production migration.

The CHIPS Act is catalyzing a domestic manufacturing resurgence with over $640 billion in private investments, though advanced-node production will remain concentrated in Taiwan and South Korea for the next 3-5 years.

Procurement professionals should evaluate not just manufacturer reputation but also supply chain reliability—component availability, lead times, technical support, and compliance with domestic sourcing requirements for defense contracts. Authorized distributors play a critical role in semiconductor procurement, offering inventory buffering, smaller order quantities, and faster delivery than direct manufacturer relationships typically provide.

While Nvidia, Intel, Qualcomm, Texas Instruments, and AMD produce cutting-edge semiconductors, specialized distributors connect manufacturers to end users. LEVEL SOLUTIONS exemplifies this role by providing:

- Immediate access to millions of components from leading suppliers

- ESD-compliant warehousing with global sourcing across billions of parts

- Support for both commercial and mil-spec applications

- Procurement solutions for automotive, aerospace, telecommunications, and industrial markets

These capabilities help procurement teams navigate supply chain complexity, allocation constraints, and technical requirements across diverse industries.

Frequently Asked Questions

What is the difference between semiconductor manufacturers and component suppliers?

Manufacturers design and fabricate chips through their own facilities or contract foundries. Suppliers and distributors procure finished chips, maintain inventory, and provide technical support and logistics that bridge manufacturers and end users.

Which U.S. semiconductor companies manufacture chips domestically?

Intel, Texas Instruments, Micron, and GlobalFoundries operate major U.S. fabs. Fabless companies like Nvidia, AMD, and Qualcomm design domestically but manufacture through TSMC (Taiwan) and Samsung (South Korea).

How has the CHIPS Act impacted U.S. semiconductor manufacturing?

The Act allocated $52.7 billion in incentives, catalyzing over $640 billion in private investment. Major awards to Intel, TSMC, Samsung, and Micron are funding new fabs across Arizona, Texas, Ohio, and New York, targeting tripled domestic capacity by 2032.

What types of semiconductors are most commonly manufactured in the U.S.?

U.S. fabs primarily produce analog chips, power semiconductors, RF components, mature logic processors, and specialty chips for automotive and defense applications. Advanced memory (DRAM) production is expanding with Micron's investments, though most cutting-edge logic chips below 7nm remain manufactured in Taiwan and South Korea.

How can companies source components from top U.S. semiconductor manufacturers?

Most manufacturers sell through authorized distributors who maintain inventory and handle logistics. Distributors like Level Solutions offer faster access, smaller order quantities, and broader availability than direct purchases, which require high minimums and longer lead times.

What are the advantages of sourcing semiconductors from U.S.-based suppliers?

Benefits include reduced geopolitical supply chain risk from Taiwan Strait tensions, compliance with domestic sourcing requirements for defense and government contracts (DFARS regulations), faster shipping and lower freight costs within North America, and support for reshoring initiatives. U.S. suppliers also offer easier access to engineering support and R&D collaboration for domestic design teams.